Record-Breaking AI-Related Debt Issuance in 2025

Authors & Contributors

Theodore Bair Jr., CFA

Bryan Steele

As cloud infrastructure providers move toward AI and data center expansion, their issuance of roughly $121 billion in new debt this year has caused investors to reassess the balance between risk and reward.

Overview of the 2025 Debt Surge

Hyperscalers – massive cloud infrastructure providers such as Amazon, Alphabet/Google, Meta, Microsoft, and Oracle1—have issued roughly $121 billion in new debt so far in 2025, with over $90 billion raised in the past three months alone. This borrowing spree has been ignited by massive expansion plans for cloud infrastructure: construction of large-scale data centers stocked with advanced servers and cutting-edge graphics processing units (GPUs), intended to satisfy the burgeoning demand for artificial intelligence (AI). These Capital Expenditure (CapEx) needs increasingly exceed expected operating cash flows, pushing firms to tap bond markets to fund growth at unprecedented speed and scale.

Impact on Credit Markets

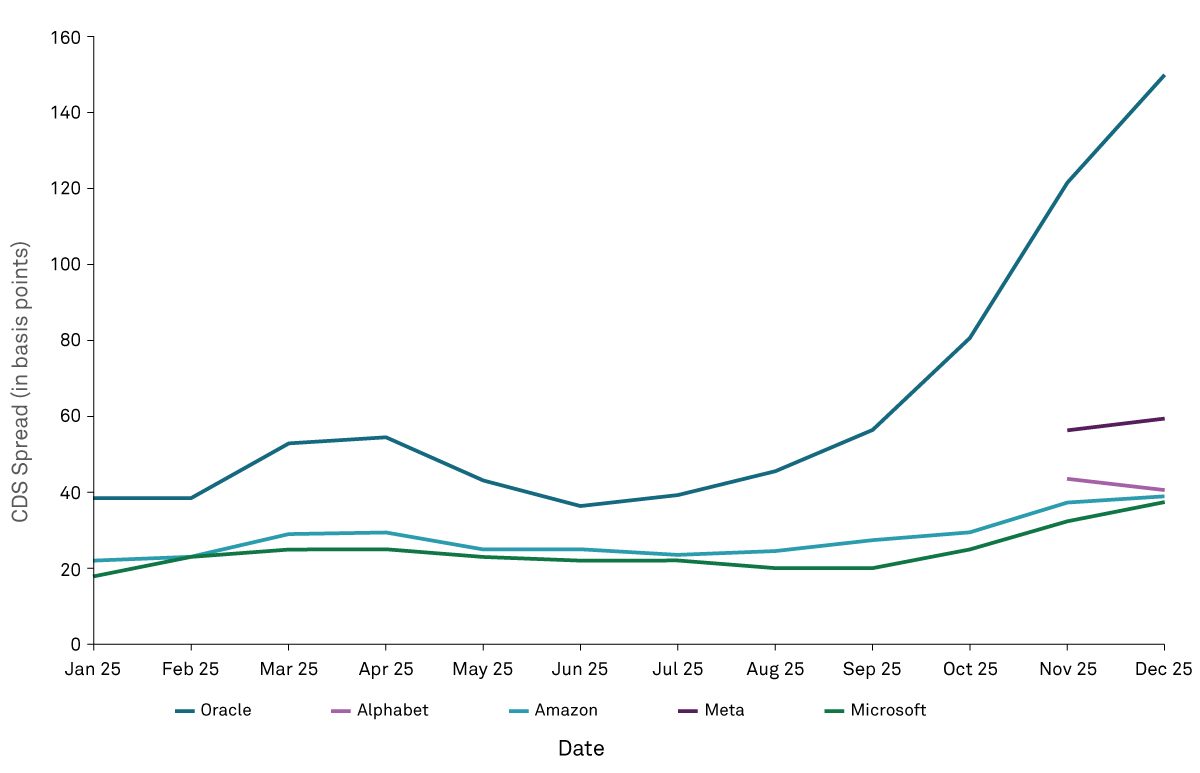

The borrowing surge has widened credit spreads, notably for Oracle and Meta, with Alphabet, Amazon, and Microsoft widening to a lesser degree. Consequently, investors are increasingly turning to credit default swaps (CDS) to hedge against the downside risks associated with AI investments. Since June, the cost of insuring hyperscaler debt through CDS has increased, reflecting heightened credit risk and increased sensitivity to the execution of substantial capital expenditure plans. As issuance accelerates and the sector's financing activities expand, we anticipate that the need to hedge exposure to AI-related investments and long-term technological liabilities will increase.

Hyperscaler 5-Year CDS Comparison

Potential for Future Debt Issuance

Wall Street firms are highlighting expectations for a continued surge in technology sector debt issuance. UBS analysts foresee as much as $900 billion in new debt from global companies in 2026. Further out, Morgan Stanley and JP Morgan project the technology sector may need to issue as much as $1.5 trillion in new debt over the next few years to finance AI and data center infrastructure construction.

Risks Associated with Hyperscaler Debt Strategies

A potential $1.5 trillion wave of AI-related bonds could strain corporate bond markets, widening spreads and heightening volatility. Parallels to the dot-com and telecom buildouts suggest risk if infrastructure returns lag expectations. An AI “CapEx bust” could pressure cash flows, trigger downgrades, and weigh on the broader economy given its growing reliance on AI-driven investment.

Mitigating Risks through Index Funds and ETFs

Passive fixed income strategies mitigate concentration through market-cap weighting with single-issuer caps and sector limits, tempering exposure even as technology issuance grows. This reduces idiosyncratic default impact and limits sector overweighting.

Investment-grade indices enforce ratings thresholds and fallen-angel rules, removing bonds downgraded below IG at scheduled rebalances, constraining exposure to weakening credits and helping maintain quality.

Routine monthly or quarterly rebalancing adds eligible new issues and removes matured or noncompliant bonds, preserving methodological discipline and preventing issuer or sector drift amid shifting issuance patterns.

ETF creation/redemption supports secondary market liquidity and helps align prices with net asset value during periods of concentrated issuance, aiding orderly absorption of large supply and facilitating tactical portfolio adjustments.

Investors can target duration bands or maturity ladders to manage interest rate and refinancing risk inherent in long-lived infrastructure financing, balancing carry against extension risk.

Navigating Opportunities and Risks

The aggressive debt issuance strategies of major hyperscalers highlight both opportunities and risks related to AI and data center expansion. While we believe infrastructure investments are essential for technological progress and economic growth, increasing leverage and the possibility of market instability underscore the need for careful risk management. Companies with strong balance sheets may be better equipped to manage financial turbulence, but sector-wide challenges could still affect even the most resilient firms. As the industry moves through this transformative period, prudent debt management and diversified investment strategies will likely be crucial for ensuring long-term stability and sustainable growth.

1Listed securities are being presented for illustrative purposes only. This is not a recommendation to buy, sell, or hold these securities. It should not be assumed that securities identified were or will be profitable or that decisions we make in the future will be profitable. Any references to specific companies are illustrative and reflect their role within broader macro or index contexts.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All investments involve risk, including the possible loss of principal. Certain investments have specific or unique risks. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

This material has been provided for informational purposes only and should not be construed as investment advice or a recommendation of any particular investment product, strategy, investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Prospective investors should consult a legal, tax or financial professional in order to determine whether any investment product, strategy or service is appropriate for their particular circumstances. This document may not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorized. Views expressed are those of the author stated and do not reflect views of other managers or the firm overall. Views are current as of the date of this publication and subject to change. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be, interpreted as recommendations. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any BNY product. Some information contained herein has been obtained from third party sources that are believed to be reliable, but the information has not been independently verified. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Indices referred to herein are used for comparative and informational purposes only and have been selected because they are generally considered to be representative of certain markets. Comparisons to indices as benchmarks have limitations because indices have volatility and other material characteristics that may differ from the portfolio, investment or hedge to which they are compared. The providers of the indices referred to herein are not affiliated with Mellon Investments Corporation (MIC), do not endorse, sponsor, sell or promote the investment strategies or products mentioned herein and they make no representation regarding the advisability of investing in the products and strategies described herein. Investors cannot invest directly in an index.