Active vs. Index Performance in H1 2025

Authors & Contributors

Over 54% of active large-cap managers underperformed the S&P 500® in H1 2025, according to Macrobond and S&P Global.

Persistent Active Underperformance, Even as Markets Shift

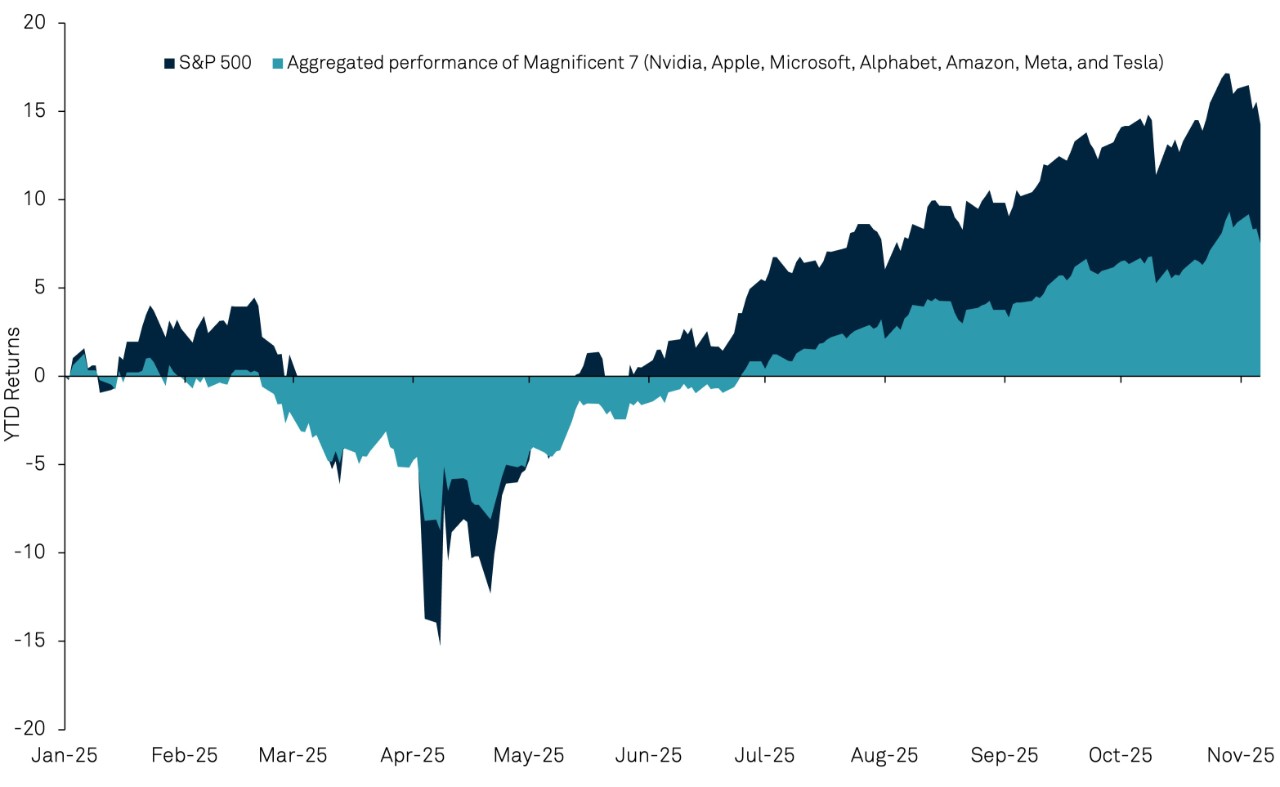

In the first half of 2025, US large-cap active managers continued to trail their benchmarks, despite an environment that seemed ripe for stock pickers. Over 54% of active large-cap strategies underperformed the S&P 500® in the first half of 2025, only modestly better than the 73% lag recorded over the full 12-month cycle. Much of the equity market’s rebound in the second quarter was concentrated in the so-called Magnificent Seven—Nvidia, Microsoft, Apple, Amazon, Alphabet, Meta and Tesla—which together represent roughly one-third of the S&P 500’s market value. Additionally, the outsized returns of the Magnificent Seven masked the poor breadth of markets in the first half of 2025, where only one in five constituents actually registered gains on days when the market advanced, leaving active portfolios struggling to keep pace.

Contribution of Magnificent 7 to S&P 500 YTD Performance

Why Index Investment Strategies “Win” More Often

Fee Drag

Active investment manager fees and trading costs potentially increase the hurdle for outperformance. In a world where index funds offer cost-effective alternatives, active strategies must generate enough alpha not only to cover these internal expenses but also to offset frictional costs such as bid-ask spreads and turnover. Even skilled active managers may find themselves in the awkward position of working solely to break even against these cost headwinds, eroding the incentive to make bold sector bets when merely matching market returns becomes a challenge.

Benchmark Construction

By design, capitalization-weighted indices aim to efficiently capture changing market dynamics, naturally maintaining exposure to stocks that have surged in price. As the Magnificent Seven continued to appreciate in the second quarter, index managers benefited from their larger index weights without any need to forecast winners. By contrast, active managers must either overweight those same names—further eroding the traditional benefits of diversification—or risk underweighting the very stocks driving total returns.

Market Efficiency & Breadth Risk

Historically, periods of extreme concentration and poor market breadth have presaged muted forward returns. Narrow rallies reduce the payoff of individual stock selection, as only a few names are responsible for most of the upside. Index investment managers aim to sidestep this risk entirely by owning the full index, eliminating the danger of stock-selection missteps that can magnify losses when only a small subset of securities is contributing to market gains.

“Always Invested” vs. “The Right Call at The Right Time”

One of the most fundamental advantages for index investment managers is that they seek to remain fully invested in the benchmark, virtually insuring the near-complete capture of returns—upside and downside alike. Active managers, by contrast, must seek to repeatedly prove their timing and conviction, entering and exiting sectors or names at precisely the right moments. Miss one major upside move or misjudge duration in a rate-sensitive environment, and a portfolio can fall behind irreversibly. Index investment managers avoid this trap entirely by owning the market continuously.

Extreme concentration in today’s large-cap markets further amplifies this edge. With a handful of mega-caps accounting for an unusually large share of returns, diversified active managers potentially find themselves either forced to overweight those same names—eroding differentiation—or watch their portfolios underperform when these stocks dominate. In many cases, the easiest way to track the index is simply to own it.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All investments involve risk, including the possible loss of principal. Certain investments have specific or unique risks. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

This material has been provided for informational purposes only and should not be construed as investment advice or a recommendation of any particular investment product, strategy, investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Prospective investors should consult a legal, tax or financial professional in order to determine whether any investment product, strategy or service is appropriate for their particular circumstances. This document may not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorized. Views expressed are those of the author stated and do not reflect views of other managers or the firm overall. Views are current as of the date of this publication and subject to change. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be, interpreted as recommendations. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any BNY Mellon product. Some information contained herein has been obtained from third party sources that are believed to be reliable, but the information has not been independently verified. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Indices referred to herein are used for comparative and informational purposes only and have been selected because they are generally considered to be representative of certain markets. Comparisons to indices as benchmarks have limitations because indices have volatility and other material characteristics that may differ from the portfolio, investment or hedge to which they are compared. The providers of the indices referred to herein are not affiliated with Mellon Investments Corporation (MIC), do not endorse, sponsor, sell or promote the investment strategies or products mentioned herein and they make no representation regarding the advisability of investing in the products and strategies described herein. Investors cannot invest directly in an index.