Déjà Vu? The Market Impacts of Brexit and United States Tariff Declaration

Authors & Contributors

Theodore Bair Jr., CFA

David Culp

Are the Trump Administration’s “Liberation Day” tariffs putting the US economy on a similar path as Brexit?

The United Kingdom’s decision to leave the European Union, commonly known as Brexit, and the announcement of extensive global tariffs by the United States have both had significant near-term (Liberation Day) and long-term (Brexit) impacts on the global economy. While the two events are distinct, they share some similarities in their market effects. In this article, we compare the market impacts of Brexit and US tariff declarations, as well as examine the reactions of the British pound sterling, US dollar (USD) and gold prices.

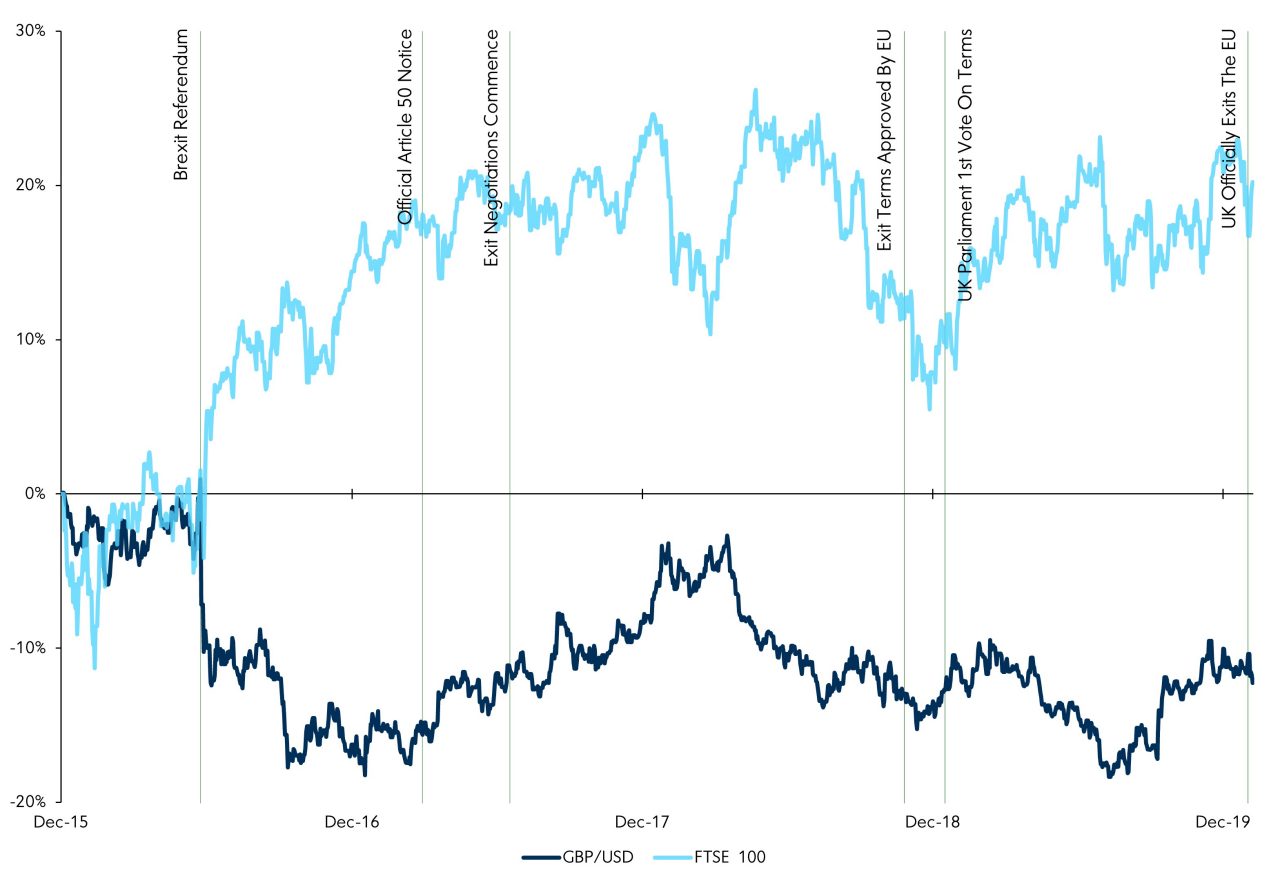

The United Kingdom’s intent to exit the European Union was officially announced in February 2016 and approved by voter referendum in June 2016, triggering a sharp decline in the pound sterling and a fall in UK equity markets. However, the FTSE 100 index recovered in short order as the weaker currency boosted exports and profitability of UK multinational companies. Defying widespread expectations of certain calamity, the UK economy showed resilience Content through the following two years with the FTSE 100 index reaching a record high in May 2018. Despite the long-running uncertainty surrounding Brexit, the UK economy and equity markets ultimately held up far better than expected.

FTSE 100 and Pound Sterling

Cumulative percent change

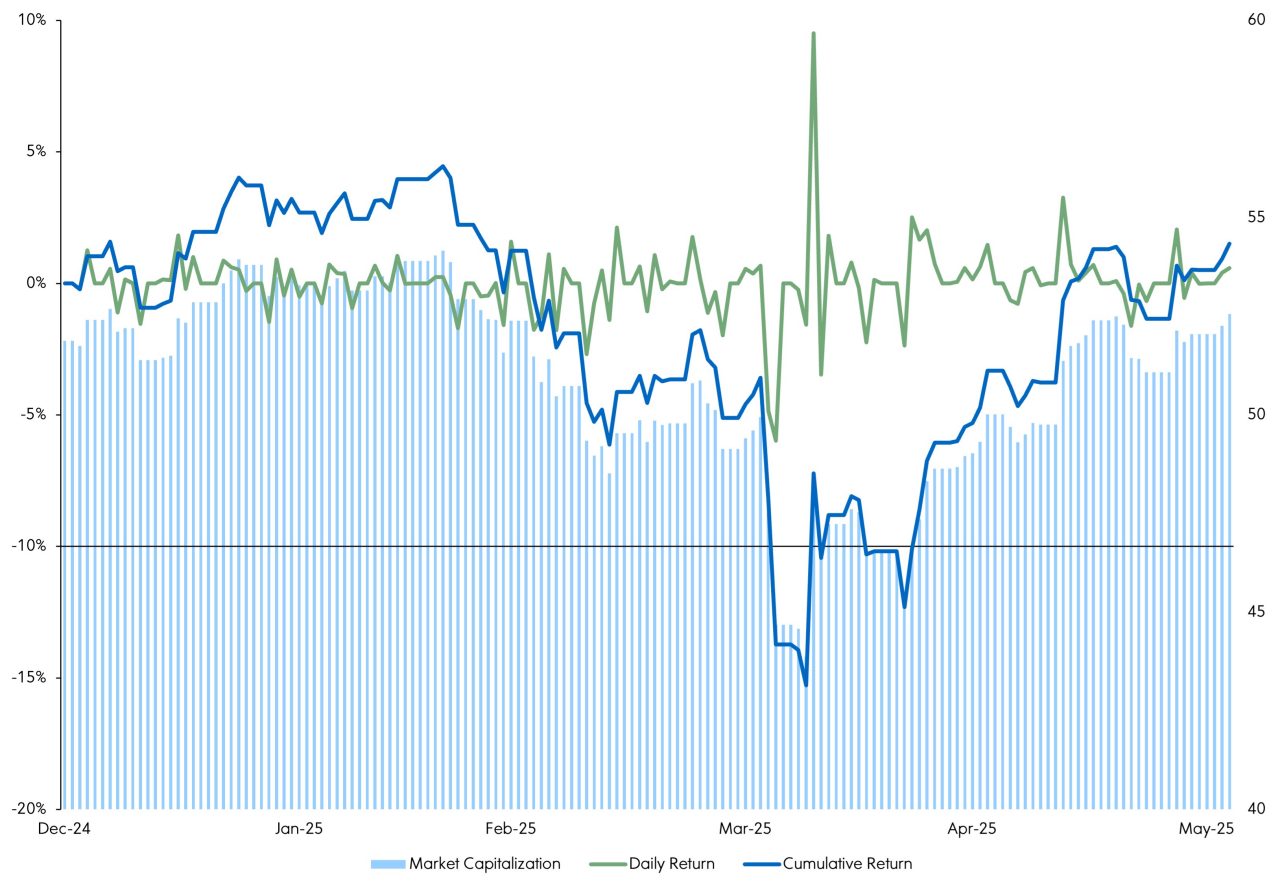

In contrast, the wide-ranging changes in trade policy pursued by the United States in the early days of the second Trump Administration has led to a more immediate and acute market reaction. The announcement on April 2, 2025, of a base tariff of 10% on virtually all US trading partners coupled with additional and sizable “reciprocal” levies on a host of countries sparked a surge in market volatility as the S&P® 500 tumbled by 10.5% while shedding over $6 trillion in market value over the subsequent two trading days. Market uncertainty was further compounded just a week later as the Trump Administration reversed course and paused most levies for 90 days. The announcement of new unilateral tariff rates on May 16, 2025, fueled further market uncertainty as investors grappled with the on-again, off-again nature of US trade policy announcements.

S&P 500 Index

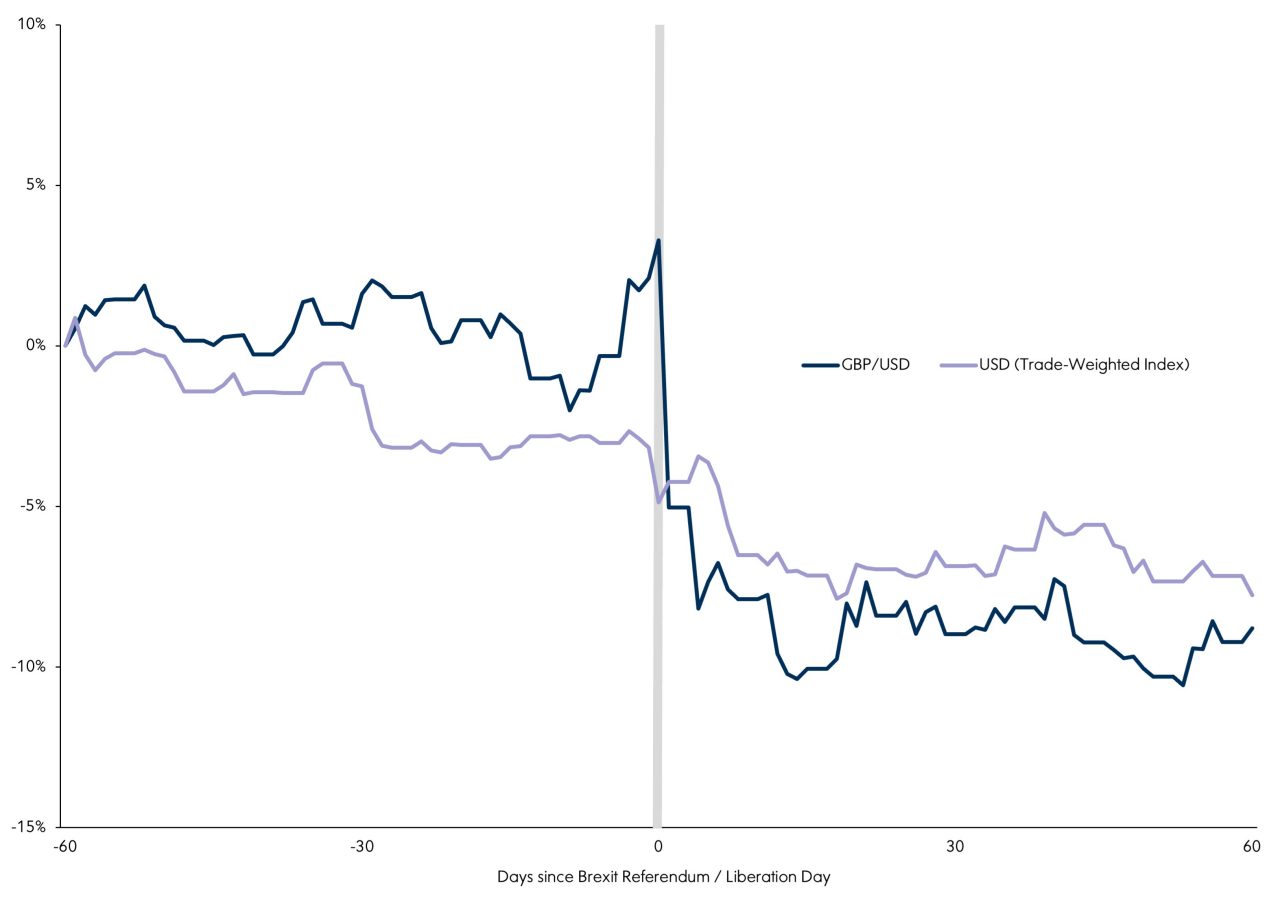

One of the key similarities between Brexit and the ongoing change in US trade policy has been the impact on currency markets. The pound sterling weakened significantly following the Brexit referendum in June 2016 and remained volatile throughout the subsequent negotiation process. Given its preeminent position in global trade, confidence in the USD began to decline several weeks prior to the April 2 “Liberation Day” announcement and has continued to depreciate as markets wrestle with the ultimate outcome of US trade policies. As can be seen in our analysis in the chart, “Pound Sterling vs. USD" (Trade-Weighted Index), both the pound sterling and the USD have followed very similar trajectories in the 60 days before and 60 days following their respective Brexit Referendum and Liberation Day events.

Pound Sterling vs. USD

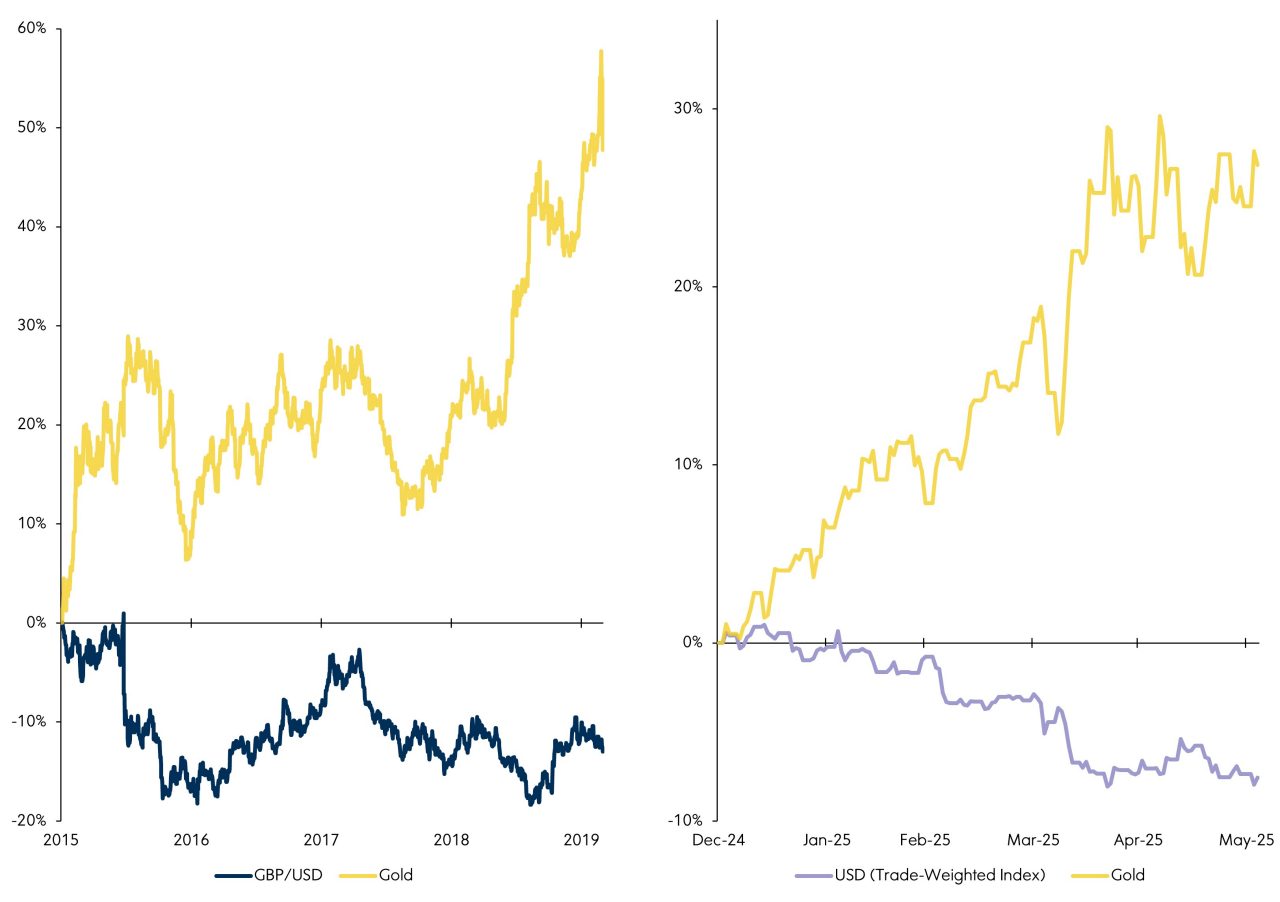

Another key similarity between Brexit and the ongoing overhaul of US trade policy can be seen in the response of gold, which often takes on the role of a safe-haven asset in times of heightened uncertainty. As can be seen in the left-hand chart below, gold prices rose sharply at the outset of Brexit while the pound sterling depreciated significantly, ultimately ending the 5- year Brexit process 10% lower. Similarly, the USD has fallen by 7.5% since the start of 2025 while gold prices have moved sharply higher. And while the depreciation of the USD has so far played out over a much shorter time horizon, the movement in gold prices have followed a similar trajectory as what occurred in the early days of Brexit, as can be seen in the right-hand chart below.

Gold and Pound Sterling | Gold and USD

Cumulative percent change

In the current environment as global trade developments continue, it is likely that we will see further market volatility and uncertainty, and it is essential to monitor the reactions of currencies and assets like gold to navigate these challenges.

Ultimately, the market impacts of Brexit and US trade policy serve as a reminder of the interconnectedness of the global economy, and the need for businesses and investors to be aware of the potential risks and opportunities that arise from major economic events. By understanding the similarities and differences between these events, we can better navigate the complexities of the global economy and make more informed decisions about our investments and business strategies.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All investments involve risk, including the possible loss of principal. Certain investments have specific or unique risks. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

This material has been provided for informational purposes only and should not be construed as investment advice or a recommendation of any particular investment product, strategy, investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Prospective investors should consult a legal, tax or financial professional in order to determine whether any investment product, strategy or service is appropriate for their particular circumstances. This document may not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorized. Views expressed are those of the author stated and do not reflect views of other managers or the firm overall. Views are current as of the date of this publication and subject to change. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be, interpreted as recommendations. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any BNY product. Some information contained herein has been obtained from third party sources that are believed to be reliable, but the information has not been independently verified. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Indices referred to herein are used for comparative and informational purposes only and have been selected because they are generally considered to be representative of certain markets. Comparisons to indices as benchmarks have limitations because indices have volatility and other material characteristics that may differ from the portfolio, investment or hedge to which they are compared. The providers of the indices referred to herein are not affiliated with Mellon Investments Corporation (MIC), do not endorse, sponsor, sell or promote the investment strategies or products mentioned herein and they make no representation regarding the advisability of investing in the products and strategies described herein. Investors cannot invest directly in an index.