Why EM Indices Belong in Portfolios

Authors & Contributors

Emerging market equities (EM) can complement US and developed market allocations by offering different growth drivers, policy cycles, and currency dynamics where the US dollar often sets the tone. A broad, disciplined index approach aims to capture macro diversification, valuation support, and currency effects over time.

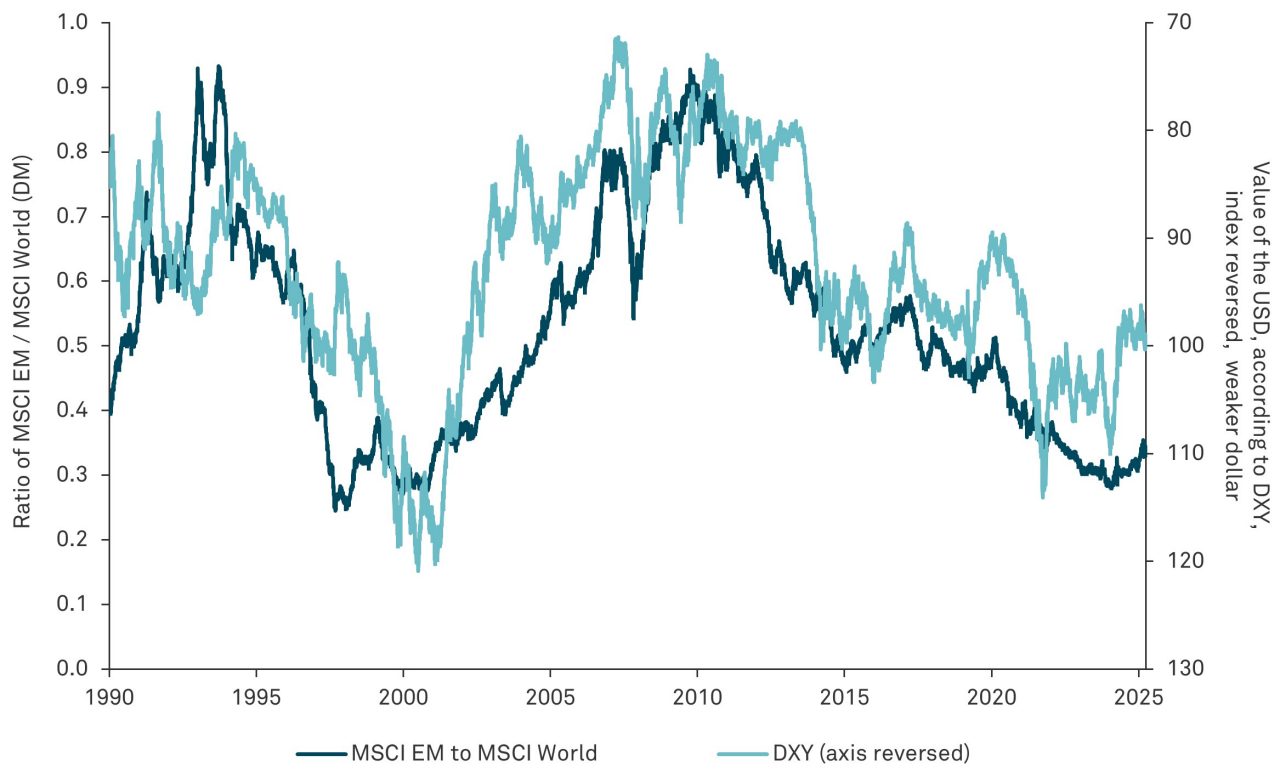

When investors consider adding EM equities to a US- or developed market-heavy portfolio, it is easy to focus on the headlines—politics, currencies and commodities. From a practical and portfolio-level perspective, EM equity index exposure reflects different growth drivers, macro and policy cycles and currency dynamics that can complement US and developed international equity allocations. The key swing factor? The US dollar.

MSCI EM / MSCI World (DM)

A strong dollar has historically been a headwind for EM, often tightening financial conditions and weighing on index-level earnings and valuations. When the dollar softens, the setup for broad EM indices tends to improve as conditions tilt toward markets where the fundamentals and policy path line up with the macro tailwinds.

Beyond the US dollar, what matters for EM index returns is how the asset class evolves structurally. Countries that are modernizing their capital markets, streamlining tax and labor rules and improving governance standards tend to experience rising market multiples over time. In our view, this is where quality shines: resilient balance sheets, consistent free cash flow and disciplined capital allocation.

Sector composition also matters. EM equities have notable exposure to commodities and greater sensitivity to global production and trade. That can be a feature, not a drawback. In periods when global manufacturing expands and capex cycles rise; those exposures add welcome diversification for portfolios dominated by US mega-cap growth sectors.

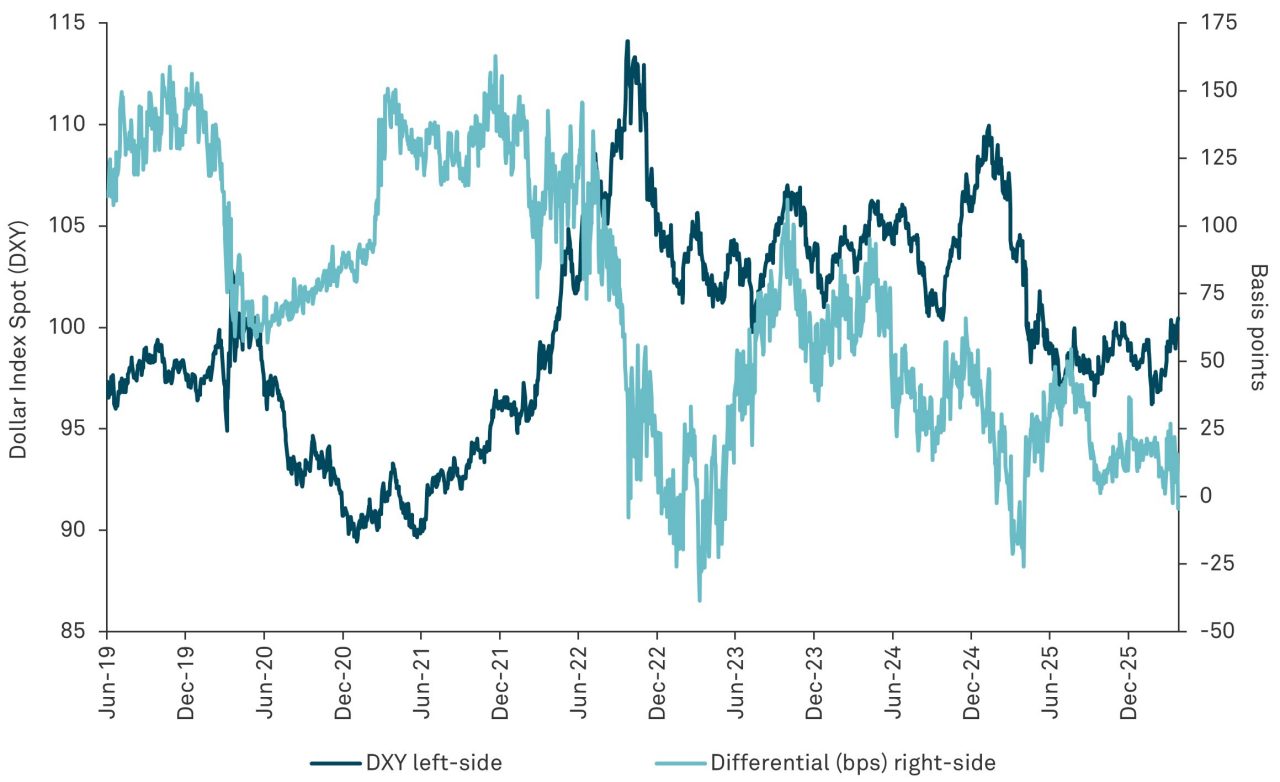

The US Dollar and Interest Rate Differentials

Valuation remains a central part of the EM case. Broad EM equities continue to trade at a discount to US equities, and a diversified index approach allows investors to access that relative value while spreading idiosyncratic risk.

Implementation should emphasize simplicity and discipline. A dedicated EM allocation expressed through broad, diversified equity indices and rebalanced periodically can integrate efficiently alongside US and developed international equity exposures, with currency treated as a structural component of returns.

Conditions that would support increased EM exposure include mild USD softness, stable global rates and improving risk appetite. Risks can include renewed dollar strength, tighter global financial conditions or a material growth shock.

Approaching EM through a broad index lens allows investors to potentially capture differentiated macro exposure, valuation support and currency diversification in a consistent and scalable way.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All investments involve risk, including the possible loss of principal. Certain investments have specific or unique risks. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

This material has been provided for informational purposes only and should not be construed as investment advice or a recommendation of any particular investment product, strategy, investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Prospective investors should consult a legal, tax or financial professional in order to determine whether any investment product, strategy or service is appropriate for their particular circumstances. This document may not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorized. Views expressed are those of the author stated and do not reflect views of other managers or the firm overall. Views are current as of the date of this publication and subject to change. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be, interpreted as recommendations. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any BNY Mellon product. Some information contained herein has been obtained from third party sources that are believed to be reliable, but the information has not been independently verified. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Indices referred to herein are used for comparative and informational purposes only and have been selected because they are generally considered to be representative of certain markets. Comparisons to indices as benchmarks have limitations because indices have volatility and other material characteristics that may differ from the portfolio, investment or hedge to which they are compared. The providers of the indices referred to herein are not affiliated with Mellon Investments Corporation (MIC), do not endorse, sponsor, sell or promote the investment strategies or products mentioned herein and they make no representation regarding the advisability of investing in the products and strategies described herein. Investors cannot invest directly in an index.