Mega IPOs and Index Rule Changes: What Index Investors Need to Know

Authors & Contributors

David Culp

Ning Chang

Robert Guldenschuh

In recent years, the interplay between natural market cyclicality and the rising sophistication of the private-to-public pipeline has led to a fundamental shift in the character of Initial Public Offerings (IPOs). Sustained by an abundance of capital earmarked for private equity, companies can now wait longer before going public, resulting in more mature companies coming to market at higher valuations than in previous cycles.

In the past, companies issuing IPOs were typically smaller and usually unfamiliar to most investors. In order to allow sufficient time for price discovery and the release of publicly available financial statements, newly public companies had to wait a minimum amount of time before being added to a benchmark, with index methodologies put in place to “promote” investor safeguards. So how does this shift towards “mega” IPOs (IPOs issued by companies worth more than $200 billion) impact public equity benchmarks and index investors? Benchmark providers are asking the same question.

Nasdaq and FTSE Russell have recently implemented faster entry timelines. However, after conducting a similar evaluation, S&P® has decided to make no changes to its methodology at this time. Faster inclusion of IPOs can make benchmarks feel timelier and more representative, but it also pulls index-tracking demand closer to the initial price discovery period, a time when the number of shares available for public trading (or “float”) may be limited and liquidity is still developing. In this essay, we break down what’s changing; why mechanics like float, weighting, and timing matter; and how those choices shape real-world execution for index-tracking portfolios.

Context and the Index Consultation Process

Benchmarks play a central role for market participants, providing vital information used to guide asset allocation decisions, identify and differentiate risks across asset classes, and measure and frame investment results. Major providers — including Nasdaq, FTSE Russell, MSCI, and S&P DJI — publish detailed rules for index construction and maintenance designed to promote market representation, investability, and transparency. However, the methodologies used by most of today’s major benchmark providers were designed in an era when new companies making the transition from private to public ownership were typically smaller, lesser-known entities with little information available to most investors.

The recent (and rapid) evolution of private markets and their ultimate intersection with public markets through the IPO process has led market participants to reconsider how newly minted companies are added to benchmarks. Today, prospective new listings can debut at significantly higher valuations than in previous cycles, raising new questions about eligibility screens, minimum float, and whether fast-entry rules should apply to all IPOs or just a subset of the largest ones. Because benchmark methodology changes can reverberate widely across asset owners, investment managers, ETF issuers, trading desks, and custodians, they are not made lightly. Instead, index providers typically follow a structured consultation process that clearly lays out the scope and impact of proposed rule changes, solicits input from market participants, and thoroughly weighs the potential benefits and risks before publishing a final decision for implementation within a clearly defined timeline.

In this light, consultations are not merely a procedural step leading to rule changes. Rather, they are an important series of checks and balances that allow practitioners to weigh a proposal’s economic and operational implications, as well as a vital mechanism by which benchmark design remains grounded in market reality instead of simply reacting to headlines and short-term trends.

Nasdaq’s proposal appeared as a public consultation in February 2026, and industry participants (including BNY) were invited to comment. FTSE Russell issued a similar consultative release in mid-February. As index managers, our role in this process is to analyze the impacts and advise our index governance committee. Ultimately, the providers incorporate input from index managers, ETF issuers, and other market experts.

An Academic Viewpoint

To evaluate the recent index sponsor proposals regarding the “fast entry” of new companies into benchmarks, it is useful to review some of the notable academic research regarding IPOs and index entries. Jay Ritter’s long-running work in this space1 has shown that IPOs, particularly smaller or speculative issues, have often underperformed comparable public companies over time. Conversely, larger and better-known IPOs are often exceptions. For instance, Ritter’s later studies suggest IPOs with more than $100 million in pre-issue sales have historically performed better than smaller, lower-revenue IPOs and, in some specifications, have performed roughly in line with the broader market. That suggests upcoming mega-IPOs might not behave as we may expect based on the average IPO.

Other research on index inclusions suggests that while such events can generate shortlived, headline-grabbing price effects, there is limited evidence of abnormal deviations in underlying values over the longer term. Robin Greenwood and Marco Sammon2 of Harvard Business School find that the S&P 500 addition premium has declined over time and is close to zero in more recent periods. A New York Fed working paper3 reaches a broadly similar conclusion, indicating that once a stock’s pre-inclusion run-up is taken into account, long-term potential returns from addition to the S&P 500 appear to be in line with established members. (The S&P 500® Index includes 500 leading US large-cap equity companies and covers approximately 80% of available market capitalization.) Studies of index rebalancing4 point to generally modest implementation costs, though these can vary meaningfully by market segment. One analysis estimates annual turnover costs at roughly 0.05% for the S&P 500 and closer to 1.5% for small-cap indexes.

Recent research from Harvard University’s Chris Murray and Marco Sammon5 examined the CRSP US indexes, comparing IPOs that were “fast-tracked” versus those that followed the normal inclusion schedule. Their findings show that fast-tracked IPOs experienced a greater-than-expected return of 5% over the inclusion window. Although this effect largely dissipates in the ensuing weeks, fast inclusion appears to shift some of the returns normally associated with the actual IPO into the index inclusion event itself. Additionally, they also show that the increased awareness of the prospect of fast entry can influence issuer behavior (i.e., when companies and underwriters anticipate early benchmark inclusion, they may adjust lockup schedules and float-related decisions accordingly). This reinforces the idea that changes in index methodology can shape not only investor outcomes but issuer incentives, as well.

Comparative Rulebook Summary

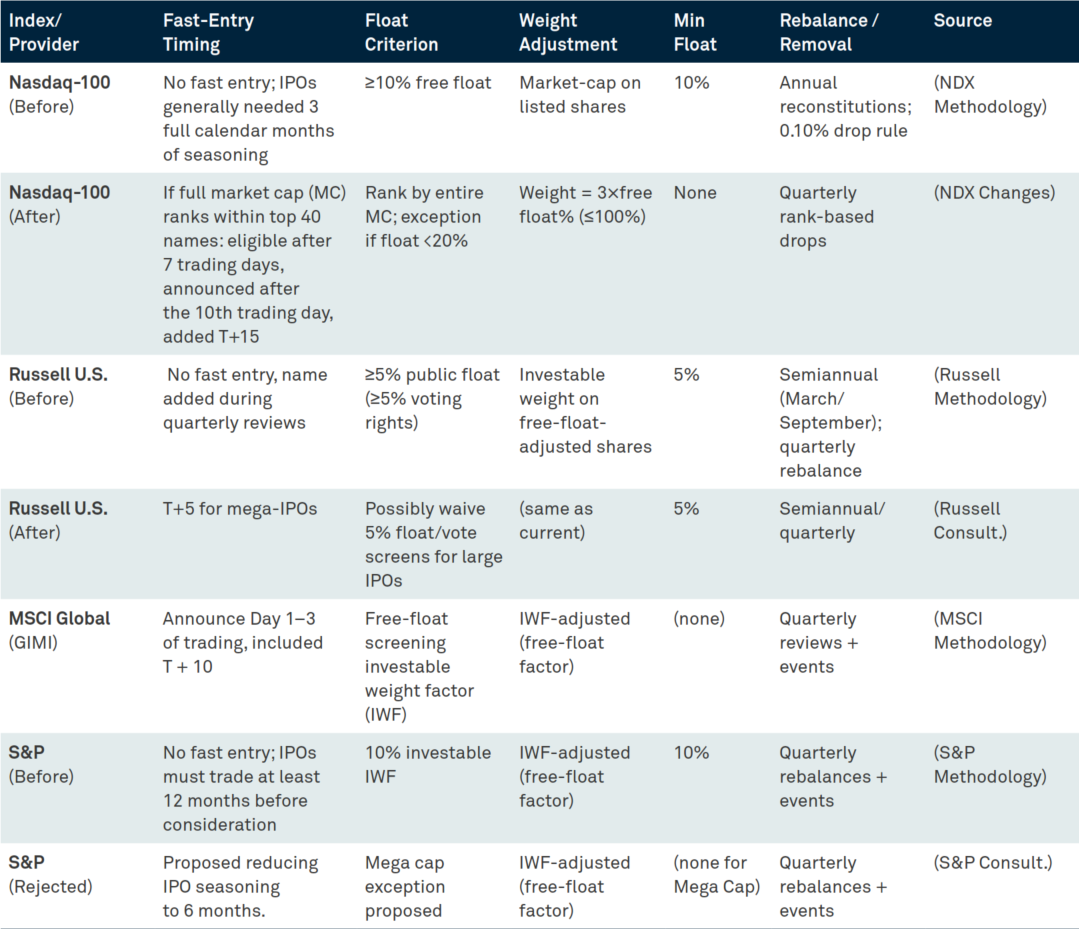

The current consultations should be understood in the context of how other index families already handle large IPOs. To put the recent Nasdaq and FTSE Russell consultations in context, we summarize the IPO practices across major index providers below:

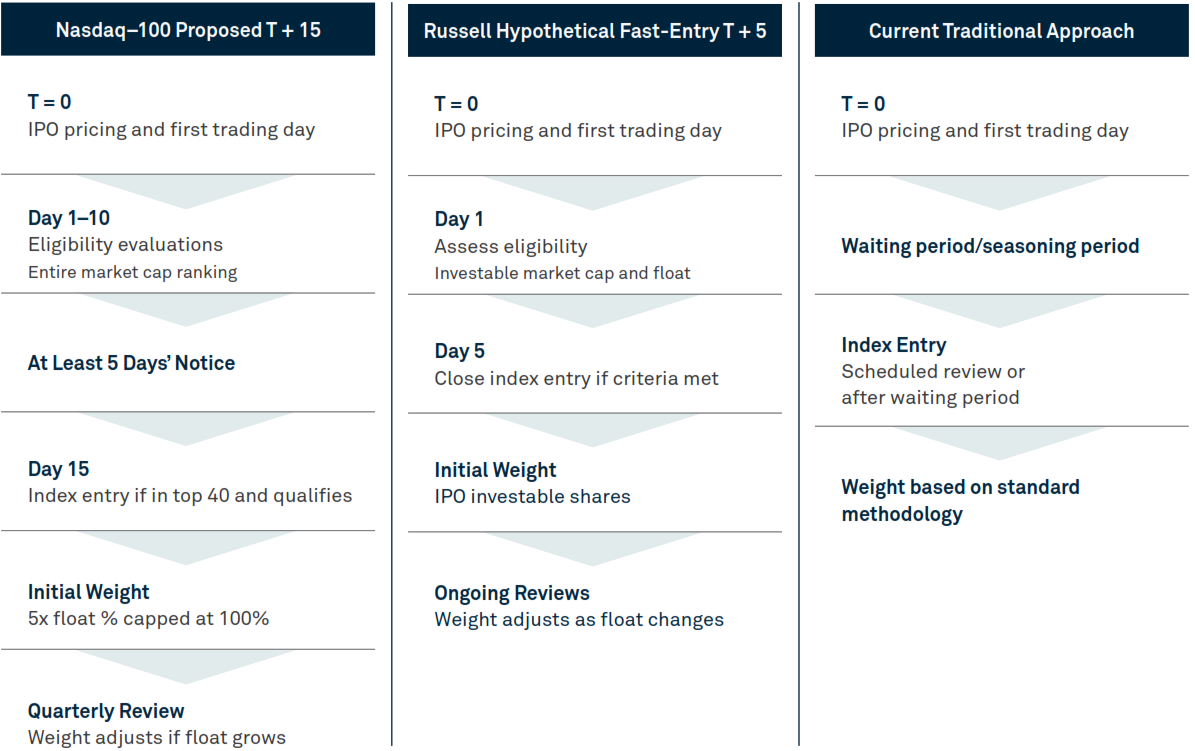

Under Nasdaq’s old methodology, new constituents typically waited at least three full calendar months of seasoning and had to meet a 10% float requirement. With Nasdaq’s recent updates, a newly listed company whose total market capitalization would rank within the top 40 current constituents could be added after 15 trading days with five days’ notice, even if the public float were much lower. The company’s initial weight would then be scaled by free float, using a 3x multiplier capped at 100%. FTSE Russell is adopting a related but distinct path in which large IPOs would enter the respective benchmark after Day 5, even if current float or voting-rights thresholds would otherwise screen them out. For example, if a $100 billion IPO has a free float of 5%, Nasdaq would give it a weight equal to 15% of its total cap ($15B initial weight). In contrast, with a full-investable-weight approach (S&P or Russell), only the $5B of float would count.

The key issue is that this is not simply a question of speed. It is also a question of what “investability” means in the context of mega-IPOs. A very large issuer may have a low float percentage but still bring a substantial dollar value of stock to market. That can be enough to qualify under a minimum investable market-cap logic (i.e., the dollar value of the company meeting the required minimum), but it does not automatically imply deep liquidity or easy execution. High dollar value and strong tradability are not equivalent. This is one reason why float percentage, investable market cap, and weighting mechanics all need to be evaluated together rather than in isolation.

Contrasting Nasdaq’s proposed 15-day inclusion rule with a hypothetical Russell 5-day inclusion rule:

How Fast-Track IPO Inclusion Could Work Across Index Providers

Potential Effects:

Here, we summarize the implications for investors in a timeline from short- to long-term:

- Short-term: When a fast-tracked IPO inclusion event occurs, index-tracking funds may need to execute sizable trades within a compressed window, which can place upward pressure on the stock price around the inclusion event. Empirical research, including the studies referenced above, generally suggests that this effect is temporary. For example, Nasdaq’s own test scenarios indicated that fast-tracked IPOs experienced an average price increase of roughly 5% on the day of inclusion. In portfolio terms, if a newly added IPO entered the index at a 1% weight and experienced a 5% abnormal price move, the resulting impact would be approximately +0.05% at the portfolio level. While modest in absolute terms, such moves can still create noticeable short-term tracking deviations.

- Medium-term: As restricted or secondary shares are released into the market over time, a company’s public float will rise, and the index weight — the percentage weight of the stock in the index based on market cap — should rise accordingly. Under Nasdaq’s proposed 3x float-adjustment framework, for example, a $200 billion company with a 5% float would initially enter the index at a $30 billion weight ($200 billion × 5% × 3). If the company’s float later increased to 10%, its index weight would rise to $60 billion. In practice, that would require index managers to make additional purchases after the initial inclusion event, extending the implementation impact beyond the IPO itself.

- Long-term (steady state): Over a sufficiently long horizon, large IPOs will be fully represented in the index whether fast-tracked or not. Put differently, the index’s long-run exposures should converge, regardless of the entry schedule; the key difference is the path and timing of that adjustment. In a fast-entry framework, very large IPOs could temporarily command outsized weights, increasing concentration in a small number of names for a notable period of time.

Throughout this timeline, the central trade-off remains between completeness of market representation and implementation practicality. While faster inclusion can improve benchmark timeliness and ensure that major new issuers are available to index investors sooner, it can also concentrate trading demand into a narrower window when float is still limited and liquidity is evolving. Over longer horizons, those effects should moderate as the companies mature and index weights normalize.

In Summary

The rise of mega-IPOs is forcing index providers to revisit assumptions that were built for a different kind of public market. Faster inclusion can make a benchmark timelier and representative of today’s economy, especially when newly listed companies are potentially large enough to rank among the larger constituents in the index. Such changes, however, have important implications for market liquidity, price discovery, and index investability. The recent index consultation process undertaken by Nasdaq, FTSE Russell, and others provides market participants with an avenue to balance these objectives and concerns, reflecting the ever-changing nature of today’s capital markets.

With over 40 years of experience managing index strategies, BNY is well positioned to navigate changes in index methodology and similar benchmark-driven events. As always, we approach such developments through a disciplined, benchmark-aware portfolio management process designed to support efficient execution while maintaining tight alignment with our benchmarks, with the ultimate goal of helping our clients achieve their long-term investment objectives.

1 Ritter, J. R. (1991). The Long-Run Performance of initial Public Offerings (pages: 3 – 27). The Journal of Finance: Volume 46, Issue 1. | Gaoa, X., Ritter, J. R., Zhu, Z. (2012). Where Have All the IPOs Gone? SEC.gov.

2 Greenwood, R., Sammon, M. (2023). The Disappearing Index Effect. Harvard Business School Revised.

3 Kasch, M., Sarkar, A. (2011, Revised 2012). Is There an S&P 500 Index Effect? Federal Reserve Bank of New York Staff Reports Staff Report No. 484.

4 Petajisto, A. (2008, Revised 2010). The Index Premium and its Hidden Cost for Index Funds. Yale SOM Working Paper No. 1235604.| Chen. H, Noronha, G., Singal, V. (2005). The Price Response to S&P 500 Index Additions and Deletions: Evidence of Asymmetry and a New Explanation (pages 1,901 – 1,930). The Journal of Finance: Volume 59, Issue 4.

5 Murry, C., Sammon, M. (2026). Primary Capital Market Transactions and Index Funds (pages 163 – 202). The Review of Asset Pricing Studies, Volume 16, Issue 2.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All investments involve risk, including the possible loss of principal. Certain investments have specific or unique risks. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

This material has been provided for informational purposes only and should not be construed as investment advice or a recommendation of any particular investment product, strategy, investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Prospective investors should consult a legal, tax or financial professional in order to determine whether any investment product, strategy or service is appropriate for their particular circumstances. This document may not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorized. Views expressed are those of the author stated and do not reflect views of other managers or the firm overall. Views are current as of the date of this publication and subject to change. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be, interpreted as recommendations. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any BNY product. Some information contained herein has been obtained from third party sources that are believed to be reliable, but the information has not been independently verified. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Indices referred to herein are used for comparative and informational purposes only and have been selected because they are generally considered to be representative of certain markets. Comparisons to indices as benchmarks have limitations because indices have volatility and other material characteristics that may differ from the portfolio, investment or hedge to which they are compared. The providers of the indices referred to herein are not affiliated with Mellon Investments Corporation (MIC), do not endorse, sponsor, sell or promote the investment strategies or products mentioned herein and they make no representation regarding the advisability of investing in the products and strategies described herein. Investors cannot invest directly in an index.

Mellon Investments Corporation (MIC) is a registered investment adviser and subsidiary of The Bank of New York Mellon Corporation (BNY). MIC is composed of two divisions; BNY Investments Mellon (Mellon), which specializes in index management, and BNY Investments Dreyfus (Dreyfus), which specializes in cash management and short duration strategies. Securities are offered through BNY Mellon Securities Corporation (BNYSC), a registered broker-dealer and affiliate of MIC. BNY Investments is the brand name for the investment management business of BNY and its investment firm affiliates worldwide.

Personnel of certain of our BNY affiliates may act as: (i) registered representatives of BNY Mellon Securities Corporation (in its capacity as a registered broker-dealer) to offer securities and certain bank-maintained collective investment funds, (ii) officers of The Bank of New York Mellon (a New York chartered bank) to offer bank-maintained collective investment funds, and (iii) Associated Persons of BNY Mellon Securities Corporation (in its capacity as a registered investment adviser) to offer separately managed accounts managed by BNY Investments firms.

MIC-947327-2026-06-03

MICA-947593-2026-06-0