India's Rise to Prominence

Authors & Contributors

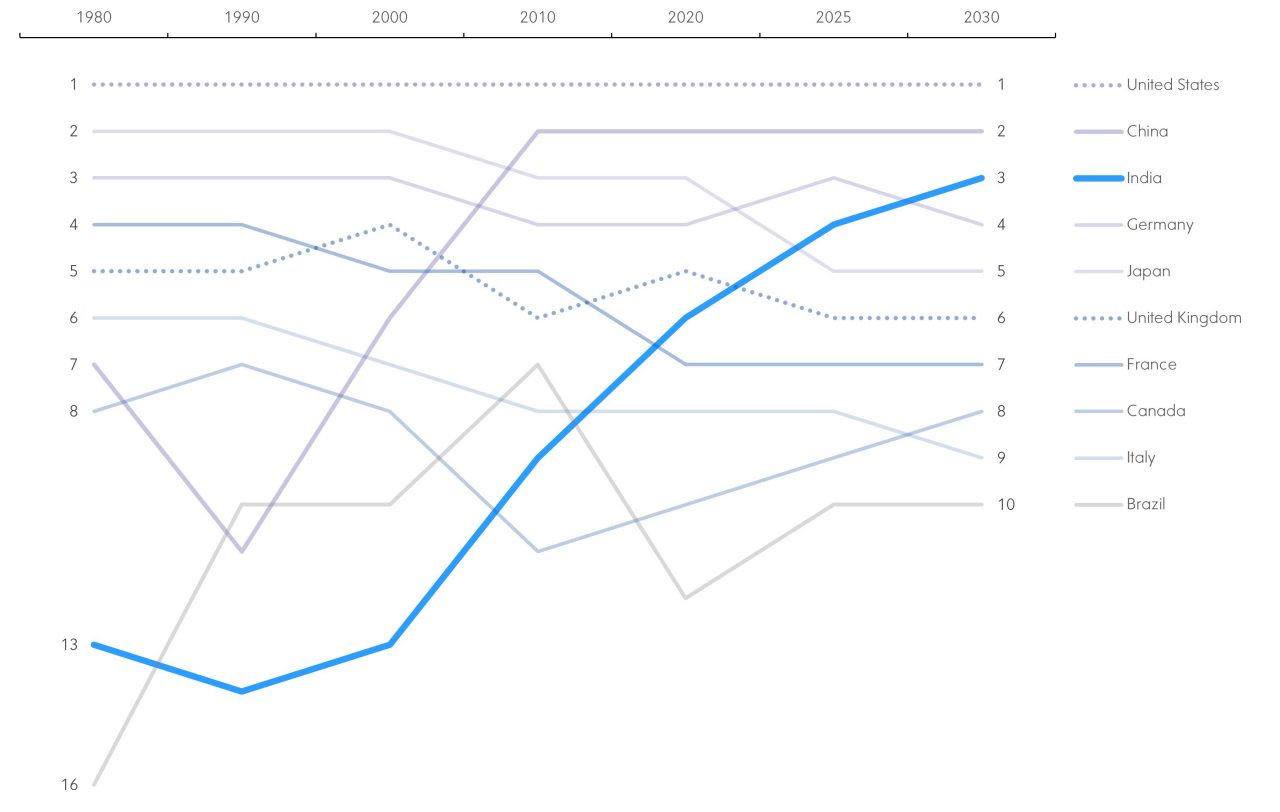

India’s economy is now the fourth largest economy in terms of nominal GDP and is expected to double its output every 11 years.

In a world of constant breaking news, India’s economy has gone under the radar and is now the world’s fourth largest economy in terms of expected nominal Gross Domestic Product (GDP) in 2025, according to the International Monetary Fund's (IMF’s) recent World Economic Outlook. India also ranked third in purchasing power terms as Indian goods and services are relatively inexpensive.

India is expected to continue growing quickly with a real-trend growth rate of 6.5% being the second fastest in the IMF's sample of 196 countries, a pace that doubles output every 11 years. Strong demographics underpin that trajectory, with India’s massive and relatively young population of over 1.4 billion people fueling growth. By the end of this decade, the IMF projects India’s economy to have surpassed both Japan and Germany in size. The two economic giants of the 20th century are growing much slower, with trend growth rates below 1%. China, the world’s second largest economy, maintains a 3.4% trend growth rate, which is less than half the pace of the past few decades as the country grapples with a shrinking population and a rebalancing of investment and consumption.

Evolution of the 10 largest economies

Global rank of nominal GDP in US dollars by year

As of mid-May, the US administration’s steep 30% tariffs on China suggest it wants to rebalance trade and rely less on their imports. However, India could be a good substitute for the US and gain ample trading opportunities. Relocating supply chains may take time, but there are signs of increased investment from large companies. For instance, a tech company recently suggested plans to shift the assembly of all of its US-sold cell phones to India by next year.

Finally, India’s rapid economic growth is reflected in its expanded presence in global benchmarks. Its share of the MSCI Emerging Markets Index has more than doubled since 2019, reaching 18.5% as of the first quarter of 2025, making it the third largest weight after China and Taiwan. As India’s economy continues to climb the ranks, it may feature as an increasingly vital component of global investment portfolios.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All investments involve risk, including the possible loss of principal. Certain investments have specific or unique risks. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

This material has been provided for informational purposes only and should not be construed as investment advice or a recommendation of any particular investment product, strategy, investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Prospective investors should consult a legal, tax or financial professional in order to determine whether any investment product, strategy or service is appropriate for their particular circumstances. This document may not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorized. Views expressed are those of the author stated and do not reflect views of other managers or the firm overall. Views are current as of the date of this publication and subject to change. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be, interpreted as recommendations. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any BNY product. Some information contained herein has been obtained from third party sources that are believed to be reliable, but the information has not been independently verified. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Indices referred to herein are used for comparative and informational purposes only and have been selected because they are generally considered to be representative of certain markets. Comparisons to indices as benchmarks have limitations because indices have volatility and other material characteristics that may differ from the portfolio, investment or hedge to which they are compared. The providers of the indices referred to herein are not affiliated with Mellon Investments Corporation (MIC), do not endorse, sponsor, sell or promote the investment strategies or products mentioned herein and they make no representation regarding the advisability of investing in the products and strategies described herein. Investors cannot invest directly in an index.