Rising Global Debt Tide

Authors & Contributors

The One, Big, Beautiful Bill Act is expected to raise the debt ceiling by $5 trillion, while the world’s other major economies face high deficits and rising debt burdens.

On July 4, the US enacted the One, Big, Beautiful Bill Act, a sweeping legislative package that reforms the tax code, trims the funding of certain federal programs and raises the debt ceiling by $5 trillion. While passing a budget through regular order may offer some reassurance to investors, the broader fiscal outlook remains troubling.

The underlying trends are concerning: tax revenues are declining relative to Gross Domestic Product (GDP), government spending continues to increase and there is little political momentum to address the growing fiscal gap. Furthermore, net interest payments make up a growing share of US government spending, an end of the era when negative real interest rates paid on government debt made the burden more manageable. According to the nonpartisan Congressional Budget Office, the new legislation is projected to add over $3 trillion to the national deficit over the next decade. This likely locks in annual deficits of 6% to 7% of GDP in coming years–roughly double the post-World War II average–and pushes the national debt toward historic highs.

However, the US is not alone in facing these fiscal pressures. High deficits and rising debt burdens are becoming a shared challenge across both advanced and emerging economies. The world’s other major economies—including Europe, Japan and China—are each grappling with their own unsustainable trends and policy dilemmas.

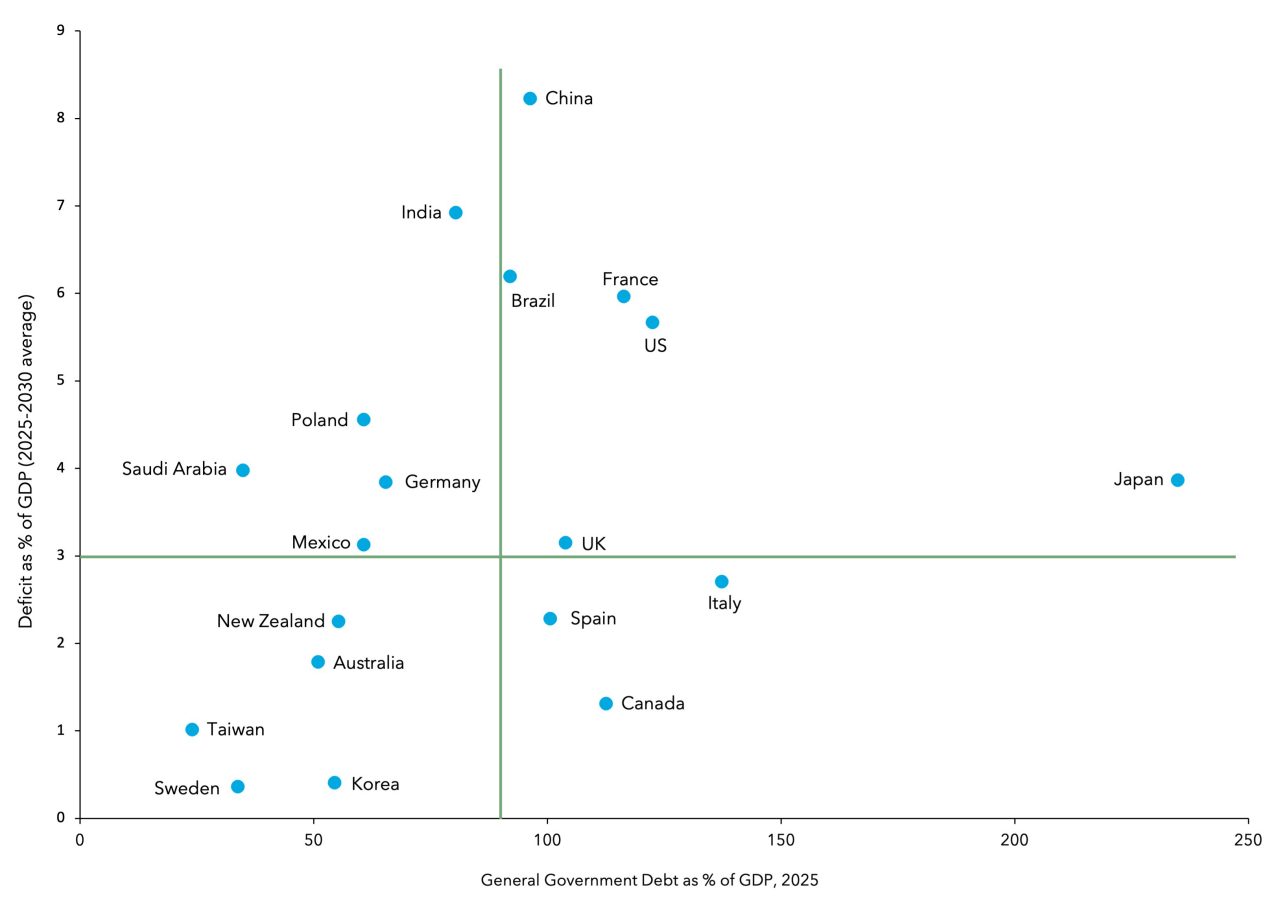

IMF Debt and Deficit Projections

In Europe, the post-Cold War model of maintaining fiscal space by minimizing defense spending under the US security umbrella—while relying on inexpensive Russian energy and Chinese imports—has been upended by geopolitics. As we discussed in our previous Macro Minute, Teutonic Shifts, Germany is re-thinking its post-Cold War fiscal stance and relaxing its constitutional debt brake to increase defense spending. Thanks to decades of fiscal discipline, Germany has a strong starting point, with headroom to grow its debt relative to its peers. France also plans to boost defense outlays, but its weaker fiscal position and fragmented political landscape pose challenges. Despite having the second-highest debt burden in our chart’s sample, Italy shows signs of improvement beneath the surface, including a primary budget surplus, reduced dependence on foreign investors and a more stable political climate.

Japan remains the most indebted major economy in terms of debt-to-GDP ratio. Its aging population and massive public debt represent a growing strain on future generations. Although most of the debt is domestically held, servicing it requires a significant transfer of resources from younger to older citizens—a burden that will intensify as the population shrinks and the Bank of Japan (BOJ) gradually normalizes interest rates.

Meanwhile, China is navigating a difficult economic transition. Its growth model has shifted from export-driven expansion to a precarious mix of real estate stimulus and fiscal support, all while demographic trends continue to worsen. The International Monetary Fund (IMF) projects that China will run deficits of around 8% of GDP for the remainder of the decade to keep its economy on track.

The broader takeaway is clear: while the US fiscal trajectory is troubling, it reflects a broader global pattern. Aging populations, geopolitical shifts and economic transitions are placing increasing pressure on public finances worldwide. As borrowing needs rise across the globe, so will the volume of marketable debt and the demand for investors willing to absorb it.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All investments involve risk, including the possible loss of principal. Certain investments have specific or unique risks. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

This material has been provided for informational purposes only and should not be construed as investment advice or a recommendation of any particular investment product, strategy, investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Prospective investors should consult a legal, tax or financial professional in order to determine whether any investment product, strategy or service is appropriate for their particular circumstances. This document may not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorized. Views expressed are those of the author stated and do not reflect views of other managers or the firm overall. Views are current as of the date of this publication and subject to change. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be, interpreted as recommendations. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any BNY Mellon product. Some information contained herein has been obtained from third party sources that are believed to be reliable, but the information has not been independently verified. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Indices referred to herein are used for comparative and informational purposes only and have been selected because they are generally considered to be representative of certain markets. Comparisons to indices as benchmarks have limitations because indices have volatility and other material characteristics that may differ from the portfolio, investment or hedge to which they are compared. The providers of the indices referred to herein are not affiliated with Mellon Investments Corporation (MIC), do not endorse, sponsor, sell or promote the investment strategies or products mentioned herein and they make no representation regarding the advisability of investing in the products and strategies described herein. Investors cannot invest directly in an index.