Tariffs as a New Revenue Stream

Authors & Contributors

According to Treasury Secretary Scott Bessent, customs duty revenues could reach $300 billion by year-end if the current tariff policies remain in place.

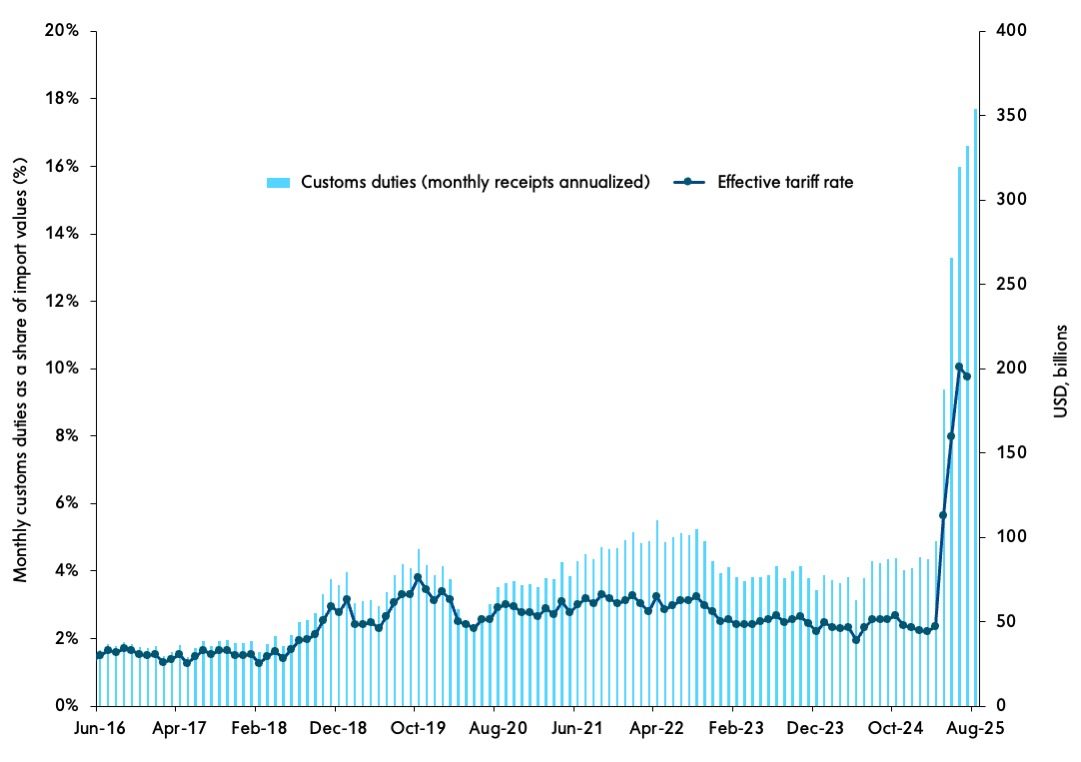

Under the Trump Administration’s expansive tariff policy, the federal government has tapped a significant new revenue stream. Through August year-to-date, $144 billion in customs duties have flowed into the Treasury, with monthly collections averaging $25 billion since the April “Liberation Day” announcement.

Treasury Secretary Scott Bessent projects that customs duty revenues could reach $300 billion by year-end if current tariffs remain in place. Meanwhile, the Congressional Budget Office (CBO) estimates that tariffs could generate $2.8 trillion over the next decade, marking a notable shift in how the federal government is funded.

Still, individual income taxes remain the dominant source of federal revenue, totaling $2.4 trillion out of the $4.7 trillion collected fiscal year-to-date. When viewed alongside income tax changes introduced in the One Big Beautiful Bill Act (OBBBA), policies suggest some of the tax burden is shifting from earnings (income tax) toward consumption (tariffs).

Federal Government Budget, Receipts, Other "Customs Duties, Total”

While tariffs increase costs in the short term, they align with the Administration’s broader industrial strategy: reshoring production and reducing reliance on foreign supply chains. Tariffs are framed not just as a revenue tool, but as a lever to strengthen domestic manufacturing and national resilience. If successful, this strategy could shift the US economy away from import-heavy consumption and toward investment in domestic production.

Importantly, historically high corporate profit margins suggest firms have room to absorb some of these costs without fully passing them on to consumers. So far, consumers have borne about 30% of the tariff burden, with the rest absorbed by firms. Many companies built up inventories earlier in the year, allowing them to delay price increases. Another surprise is that foreign exporters have absorbed virtually none of the tariff costs, according to import price data. We believe this is temporary and that more inflation passthrough is likely in the months ahead.

As for the inflationary impact, a broad tariff package consistent with the Administration’s announcements could add about one percentage point to inflation within a year, primarily as a one-time upward shift in the price level. However, if firms and workers begin to embed these higher costs into their expectations, the inflationary effects could become more persistent—potentially prompting the Federal Reserve (Fed) to reassess its monetary policy stance.

Tariffs are inherently regressive, disproportionately affecting lower-income households that spend a larger share of their income on goods. If tariffs succeed in structurally reducing imports, customs revenue may eventually decline. Once embedded in the revenue mix, tariffs may be politically difficult to unwind, especially in an era of high government debt.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All investments involve risk, including the possible loss of principal. Certain investments have specific or unique risks. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

This material has been provided for informational purposes only and should not be construed as investment advice or a recommendation of any particular investment product, strategy, investment manager or account arrangement, and should not serve as a primary basis for investment decisions. Prospective investors should consult a legal, tax or financial professional in order to determine whether any investment product, strategy or service is appropriate for their particular circumstances. This document may not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorized. Views expressed are those of the author stated and do not reflect views of other managers or the firm overall. Views are current as of the date of this publication and subject to change. This information may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or expectations will be achieved, and actual results may be significantly different from that shown here. The information is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be, interpreted as recommendations. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any BNY Mellon product. Some information contained herein has been obtained from third party sources that are believed to be reliable, but the information has not been independently verified. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Indices referred to herein are used for comparative and informational purposes only and have been selected because they are generally considered to be representative of certain markets. Comparisons to indices as benchmarks have limitations because indices have volatility and other material characteristics that may differ from the portfolio, investment or hedge to which they are compared. The providers of the indices referred to herein are not affiliated with Mellon Investments Corporation (MIC), do not endorse, sponsor, sell or promote the investment strategies or products mentioned herein and they make no representation regarding the advisability of investing in the products and strategies described herein. Investors cannot invest directly in an index.